Brief Introducation to JAGS and R2jags in R

This post is aimed to introduce the basics of using jags in R programming. Jags is a frequently used program for conducting Bayesian statistics.Most of information below is borrowed from Jeromy Anglim’s Blog. I will keep editing this post if I found more resources about jags.

1 What is JAGS?

JAGS stands for Just Another Gibbs Sampler. To quote the program author, Martyn Plummer, “It is a program for analysis of Bayesian hierarchical models using Markov Chain Monte Carlo (MCMC) simulation…” It uses a dialect of the BUGS language, similar but a little different to OpenBUGS and WinBUGS.

2 Installation

To run jags with R, There is an interface with R called rjags.

1. Download and install Jags based on your operating system.

2. Install additional R packages: type in install.packages(c(“rjags”,”coda”)) in R console. rjags is to interface with JAGS and coda is to process MCMC output.

3 JAGS Examples

There are a lot of examples online. The following provides links or simple codes to JAGS code.

- Justin Esarey

- An entire course on Bayesian Statistics with examples in R and JAGS. It includes 10 lectures and each lecture lasts around 2 hours. The content is designed for a social science audience and it includes a syllabus linking with Simon Jackman’s text. The videos are linked from above or available direclty on YouTube.

- Jeromy Anglim

- The author of this blog also provides a few examples. He shared the codes on his github account

- John Myles White

- A course on statistical models that is under development with JAGS scripts on github.

- Simple introductory examples of fitting a normal distribution, linear regression, and logistic regression

- A follow-up post demonstrating the use of the coda package with rjags to perform MCMC diagnostics.

- A simple simulation sample:

First, simulate the Data:

Next, we create the outcome y based on coefficients b_1 and b_2 for the respective predictors and an intercept a:

b1 <- 1.2

b2 <- -3.1

a <- 1.5

y <- b1*x1 + b2*x2 + eNow, we combine the variables into one dataframe for processing later:

sim.dat <- data.frame(y, x1, x2)And we create and summarize a (frequentist) linear model fit on these data:

Call:

lm(formula = y ~ x1 + x2, data = sim.dat)

Residuals:

Min 1Q Median 3Q Max

-1.3432 -0.6797 -0.1112 0.5367 3.2304

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.34949 0.28810 1.213 0.228

x1 1.13511 0.05158 22.005 <2e-16 ***

x2 -3.09361 0.20650 -14.981 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.9367 on 97 degrees of freedom

Multiple R-squared: 0.8772, Adjusted R-squared: 0.8747

F-statistic: 346.5 on 2 and 97 DF, p-value: < 2.2e-163.1 Beyesian Model

Now define the vectors of the data matrix for JAGS:

y <- sim.dat$y

x1 <- sim.dat$x1

x2 <- sim.dat$x2

N <- nrow(sim.dat)Read in the data frame for JAGS

sim.dat.jags <- list("y", "x1", "x2", "N")Define the parameters whose posterior distributions you are interested in summarizing later:

bayes.mod.params <- c("alpha", "beta1", "beta2")Setting up starting values

bayes.mod.inits <- function(){

list("alpha" = rnorm(1), "beta1" = rnorm(1), "beta2" = rnorm(1))

}

# inits1 <- list("alpha" = 0, "beta1" = 0, "beta2" = 0)

# inits2 <- list("alpha" = 1, "beta1" = 1, "beta2" = 1)

# inits3 <- list("alpha" = -1, "beta1" = -1, "beta2" = -1)

# bayes.mod.inits <- list(inits1, inits2, inits3)3.2 Fitting the model

set.seed(123)

bayes.mod.fit <- jags(data = sim.dat.jags, inits = bayes.mod.inits,

parameters.to.save = bayes.mod.params, n.chains = 3, n.iter = 9000,

n.burnin = 1000, model.file = bayes.mod)module glm loadedCompiling model graph

Resolving undeclared variables

Allocating nodes

Graph information:

Observed stochastic nodes: 100

Unobserved stochastic nodes: 4

Total graph size: 511

Initializing model3.3 Diagnostics

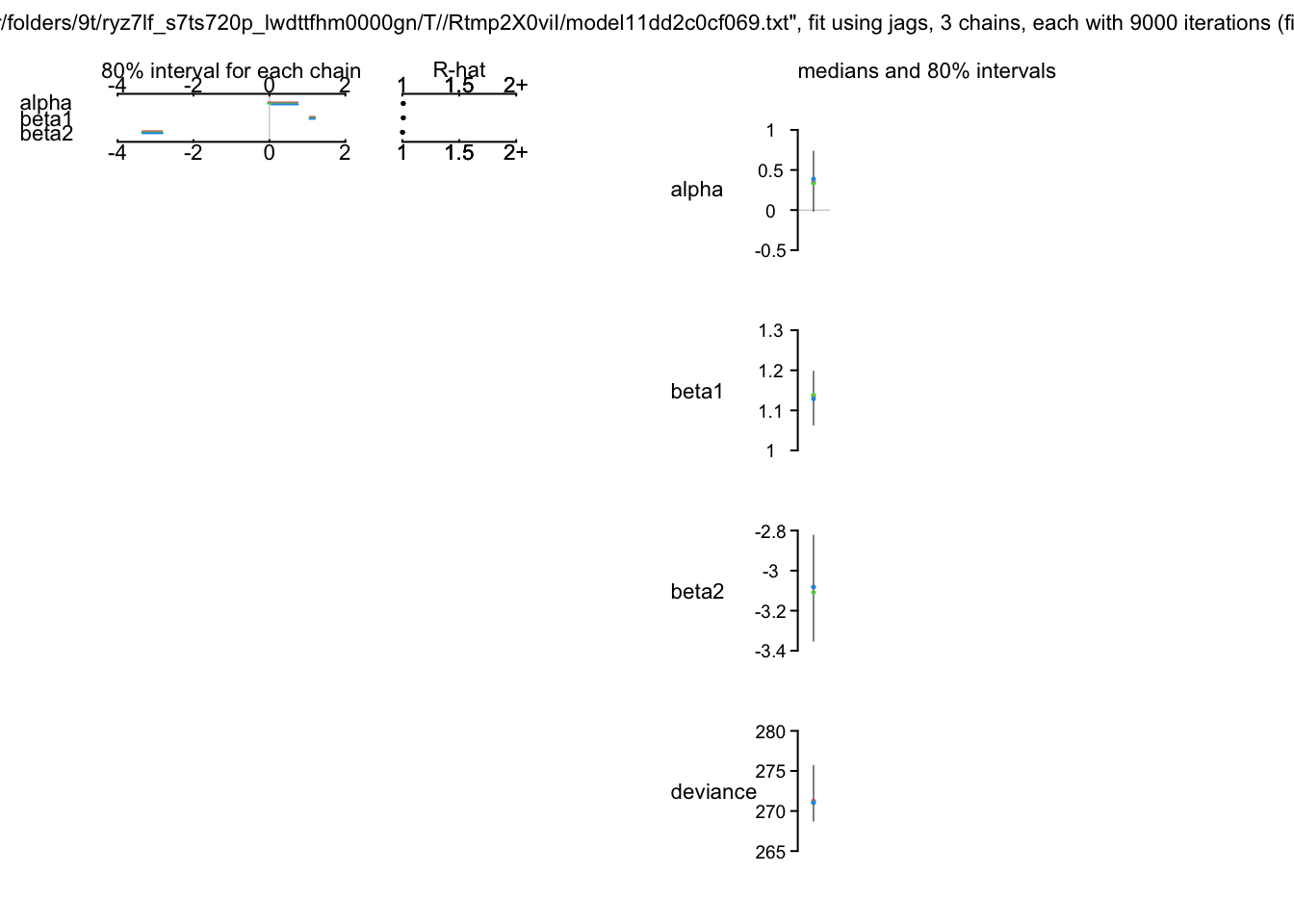

print(bayes.mod.fit)Inference for Bugs model at "/var/folders/9t/ryz7lf_s7ts720p_lwdttfhm0000gn/T//Rtmp2X0viI/model11dd2c0cf069.txt", fit using jags,

3 chains, each with 9000 iterations (first 1000 discarded), n.thin = 8

n.sims = 3000 iterations saved

mu.vect sd.vect 2.5% 25% 50% 75% 97.5% Rhat n.eff

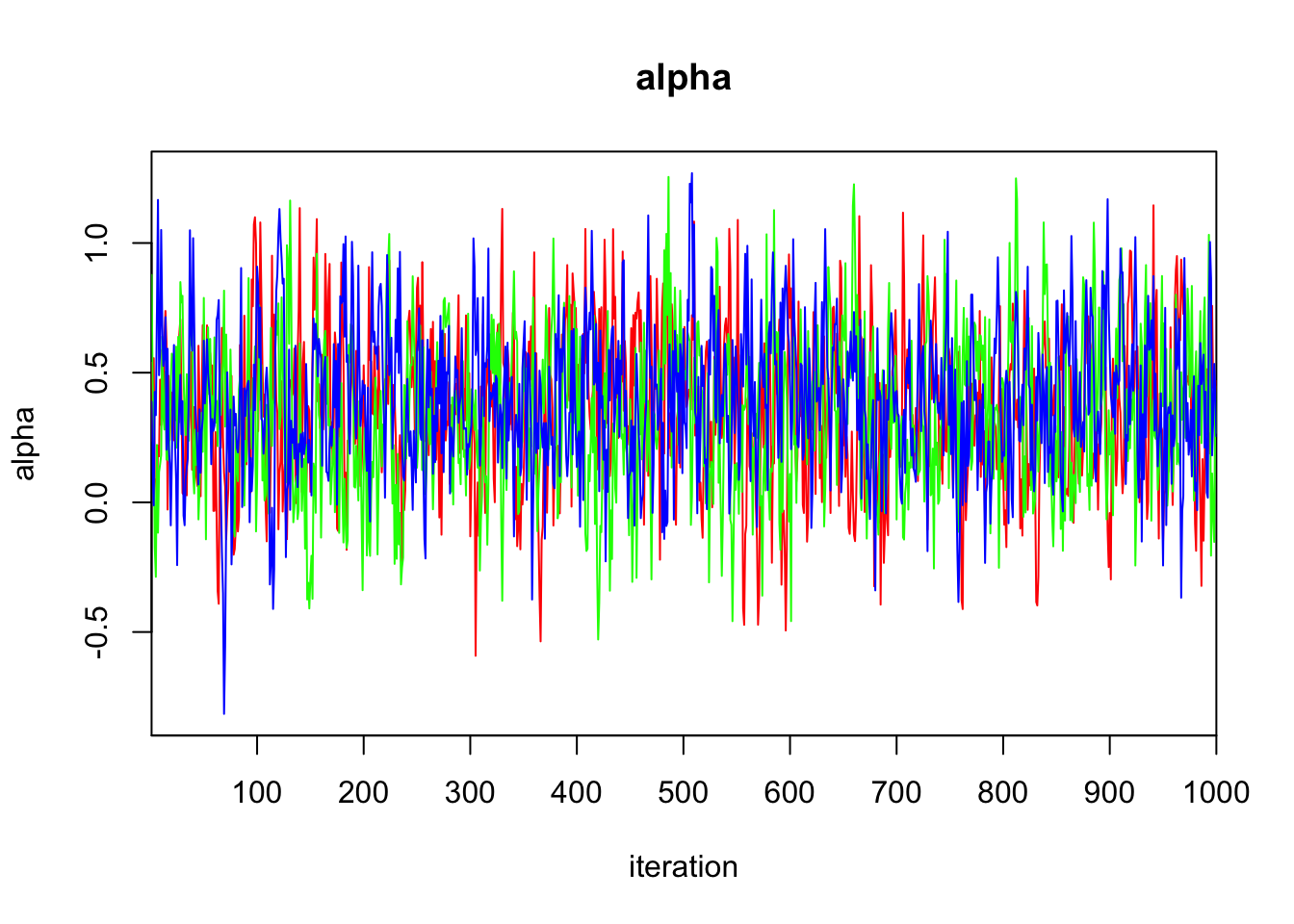

alpha 0.362 0.293 -0.205 0.166 0.358 0.562 0.958 1.009 250

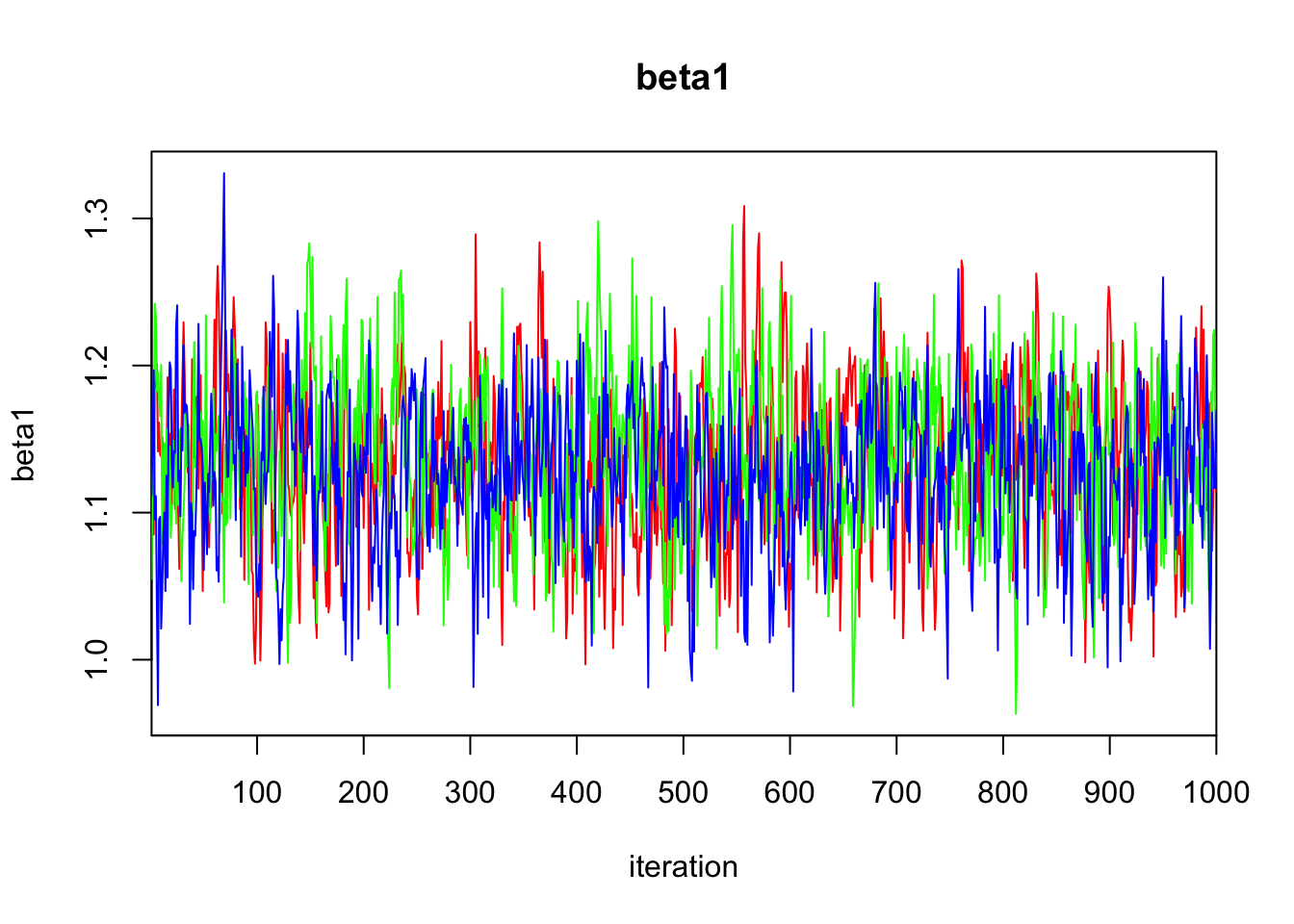

beta1 1.133 0.053 1.025 1.099 1.134 1.169 1.236 1.009 250

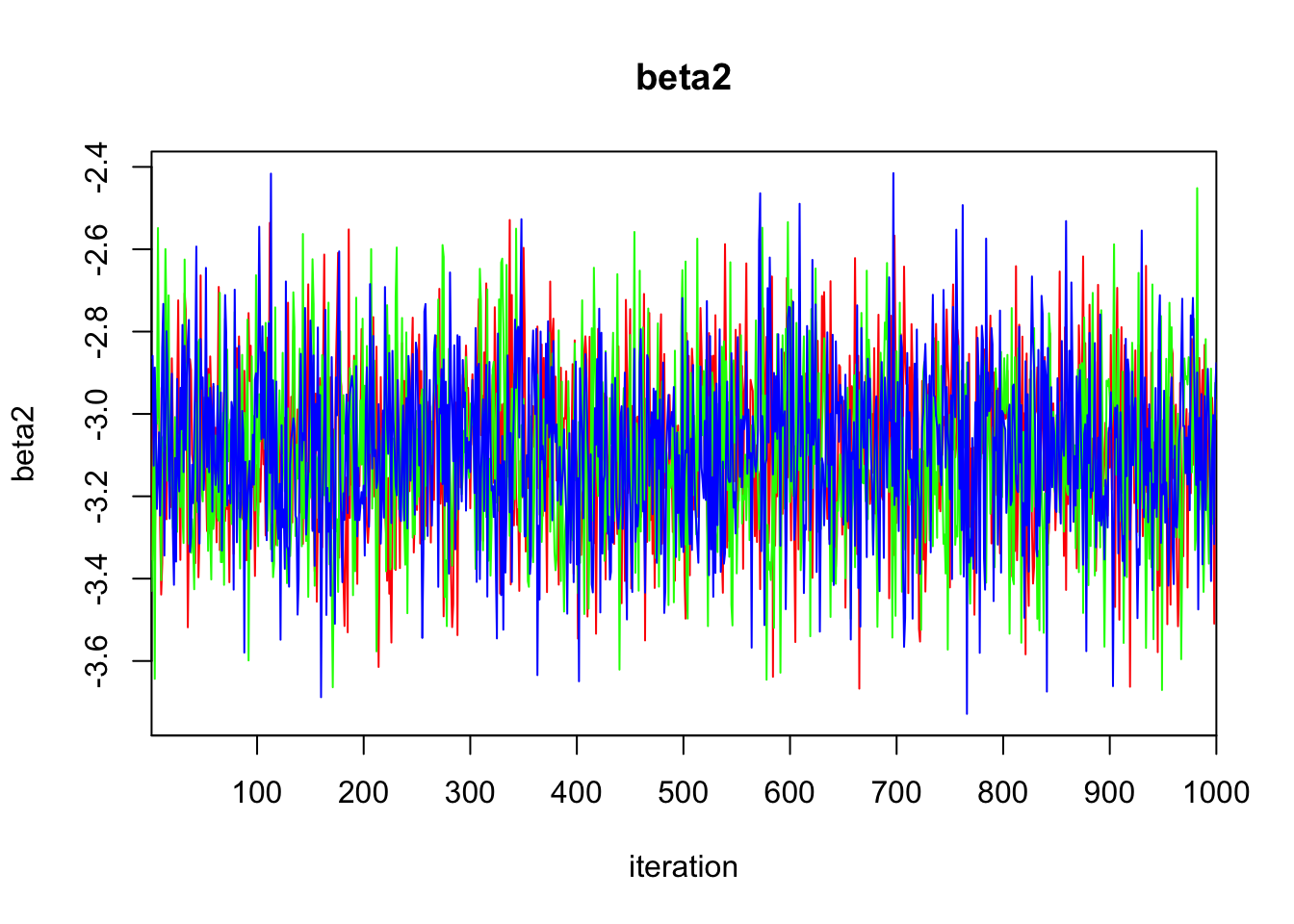

beta2 -3.090 0.205 -3.496 -3.231 -3.090 -2.950 -2.685 1.002 1700

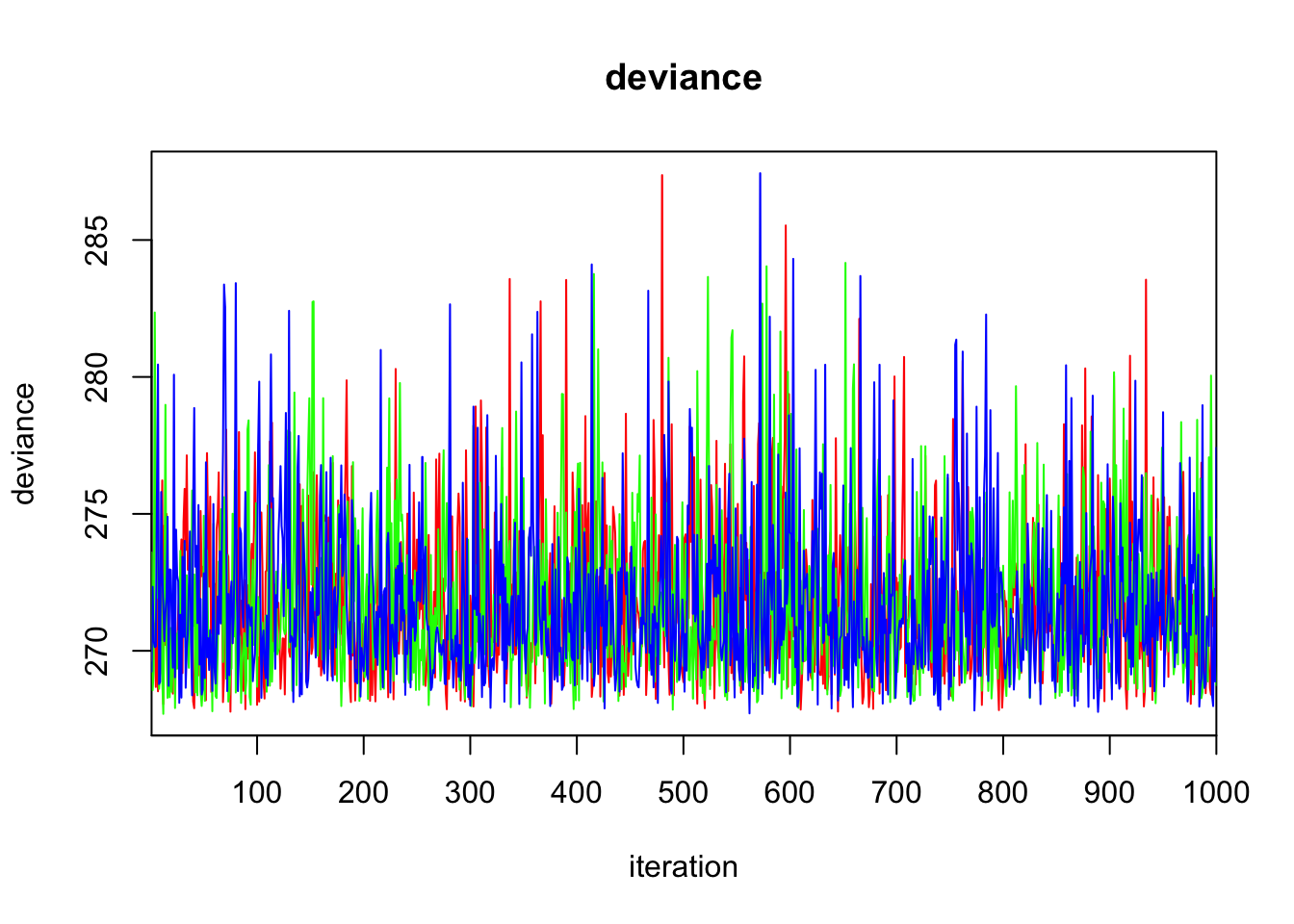

deviance 271.830 2.899 268.167 269.718 271.122 273.198 279.223 1.000 3000

For each parameter, n.eff is a crude measure of effective sample size,

and Rhat is the potential scale reduction factor (at convergence, Rhat=1).

DIC info (using the rule, pD = var(deviance)/2)

pD = 4.2 and DIC = 276.0

DIC is an estimate of expected predictive error (lower deviance is better).plot(bayes.mod.fit)

traceplot(bayes.mod.fit)